Loans that normally have repayment terms of 15, 20, or 30 years. Both the rates of interest and the month-to-month payments (for principal and interest) stay the very same during the life of the loan. The rate spent for obtaining money, normally mentioned in percentages and as an annual rate. Fees charged by the loan provider for processing a loan; frequently revealed as a percentage of the loan quantity.

Often the agreement also specifies the variety of points to be paid at closing. A contract, signed by a borrower when a home mortgage is made, that offers the lending institution the right to acquire the residential or commercial property if the customer fails to pay off, or defaults on, the loan.

Loan officers and brokers are often permitted to keep some or all of this difference as extra compensation. (likewise called discount points) One point is equal to 1 percent of the principal amount of a mortgage loan. For example, if a mortgage is $200,000, one point equates to $2,000. Lenders frequently charge points in both fixed-rate and variable-rate mortgages to cover loan origination costs or to offer extra payment to the loan provider or broker.

In many cases, the https://www.bloomberg.com/press-releases/2019-12-19/record-numbers-of-consumers-continue-to-ask-wesley-financial-group-to-assist-in-timeshare-debt-relief cash required to pay points can be borrowed, but increases the loan quantity and the overall costs. Discount points (often called discount rate fees) are points that the borrower willingly chooses to pay in return for a lower interest rate. Safeguards the lending institution versus a loss if a borrower defaults on the loan.

When you get 20 percent equity in your house, PMI is cancelled. Depending on the size of your home loan and deposit, these premiums can add $100 to $200 each month or more to your payments. Fees paid at a loan closing. Might include application fees; title evaluation, abstract of title, title insurance, and residential or commercial property study fees; charges for preparing deeds, home mortgages, and settlement documents; lawyers' costs; recording costs; estimated expenses of taxes and insurance; and notary, appraisal, and credit report fees.

What Does What Are The Current Interest Rates On Mortgages Mean?

The excellent faith price quote lists each expected cost either as a quantity or a variety. Browse this site A term typically describing savings banks and savings and loan associations. Board of Governors of the Federal Reserve System Department of Real Estate and Urban Advancement Department of Justice Department of the Treasury Federal Deposit Insurance Coverage Corporation Federal Real Estate Finance Board Federal Trade Commission National Cooperative Credit Union Administration Office of Federal Housing Enterprise Oversight Office of the Comptroller of the Currency Office of Thrift Supervision These agencies (except the Department of the Treasury) enforce compliance with laws that forbid discrimination in loaning.

Eager to take advantage of traditionally low interest rates and purchase a home? Getting a home mortgage can constitute your biggest and most meaningful financial transaction, but there are a number of actions associated with the procedure. Your credit report informs loan providers just how much you can be trusted to repay your mortgage on time and the lower your credit history, the more you'll pay in interest." Having a strong credit rating and credit rating is necessary due to the fact that it implies you can receive favorable rates and terms when obtaining a loan," states Rod Griffin, senior director of Public Education and Advocacy for Experian, among the three major credit reporting firms.

Bring any past-due accounts present, if possible. Evaluation your credit reports free of charge at AnnualCreditReport. com in addition to your credit report (often available devoid of your charge card or bank) a minimum of 3 to 6 months before obtaining a home loan. When you receive your credit rating, you'll get a list of the leading factors affecting your rating, which can tell you what modifications to make to get your credit in shape.

Contact the reporting bureau immediately if you find any. It's fun to fantasize about a dream home with all the trimmings, however you ought to attempt to only acquire what you can reasonably pay for." Most experts believe you need to not spend more than 30 percent of your gross monthly income on home-related expenses," says Katsiaryna Bardos, associate professor of finance at Fairfield University in Fairfield, Connecticut.

This is identified by summing up all of your monthly debt payments and dividing that by your gross monthly income." Fannie Mae and Freddie Mac loans accept an optimum DTI ratio of 45 percent. If your ratio is greater than that, you might want to wait to buy a home up until you lower your debt," Bardos recommends.

The Best Guide To How Do Down Payments Work On Mortgages

You can determine what you can pay for by utilizing Bankrate's calculator, which elements in your income, regular monthly commitments, approximated down payment, the details of your home mortgage like the interest rate, and house owners insurance coverage and property taxes. To be able to manage your month-to-month real estate costs, which will include payments toward the mortgage principal, interest, insurance coverage and taxes in addition to upkeep, you ought to prepare to salt away a large amount.

One general guideline of thumb is to have the equivalent of roughly six months of mortgage payments in a cost savings account, even after you hand over the down payment. Don't forget that closing expenses, which are the fees you'll pay to close the mortgage, typically run between 2 percent to 5 percent of the loan principal - who took over taylor bean and whitaker mortgages.

In general, aim to save as much as possible till you reach your desired deposit and reserve cost savings objectives." Start little if needed however stay committed. Try to prioritize your savings before spending on any discretionary products," Bardos advises. "Open a separate account for down payment cost savings that you do not utilize for any other costs.

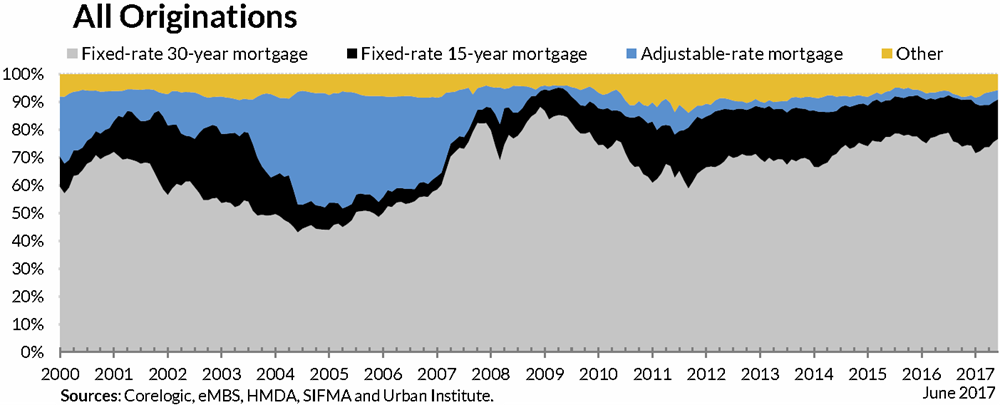

The primary types of home mortgages consist of: Traditional loans Government-insured loans (FHA, USDA or VA) Jumbo loans These can be either fixed- or adjustable-rate, implying the interest rate is either fixed throughout of the loan term or changes at predetermined intervals - what credit score do banks use for mortgages. They frequently can be found in 15- or 30-year terms, although there may be 10-year, 20-year, 25-year or even 40-year mortgages available.

5 percent down. To find the ideal lender, "talk with buddies, relative and your agent and request for referrals," recommends Guy Silas, branch manager for the Rockville, Maryland workplace of Embrace Home Loans. "Likewise, look on rating websites, carry out internet research and invest the time to genuinely read customer evaluations on lenders." [Your] choice ought to be based upon more than simply cost and interest rate," nevertheless, says Silas.

The smart Trick of How Do Mortgages Work In Canada That Nobody is Talking About

Early while doing so, it's also an excellent concept to get preapproved for a home loan. With a preapproval, a lending institution has determined that you're creditworthy based on your financial picture, and has actually issued a preapproval letter suggesting it wants to lend you a specific quantity for a mortgage." Getting preapproved https://www.nashvillepost.com/business/development/commercial-real-estate/article/21080797/williamson-timeshare-exit-business-fights-for-credibility-in-murky-industry prior to going shopping for a house is best since it suggests you can place a deal as quickly as you find the ideal home," Griffin says (why reverse mortgages are a bad idea).

Getting preapproved is likewise crucial since you'll know exactly just how much money you're authorized to obtain." With preapproval in hand, you can start seriously looking for a home that meets your needs. Make the effort to browse for and pick a home that you can visualize yourself living in. When you discover a home that has the ideal blend of cost and livability, however, strike quickly.